The 5-Minute Rule for Get A USDA Loan - Trusted USDA RD Loan Lenders

Intro to USDA Rural Development Home Loans - Fifth Third Bank

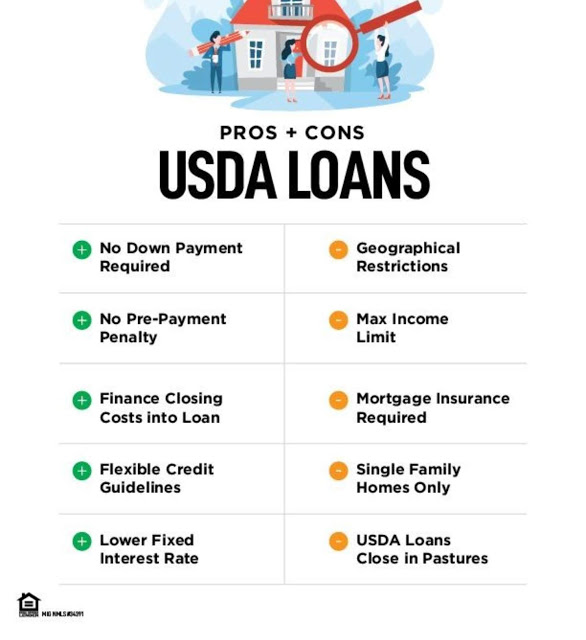

An Unbiased View of Eligibility Requirements for USDA Loans - Do you qualify?

The objective declaration of the USDA home mortgage program is "to improve the economy and quality of life in rural America." It was created by the U.S. Department of Agriculture to help low and really low income applicants in acquiring good, safe, and hygienic housing in eligible backwoods. The housing provisions set in motion by the USDA mortgage program motivated rural homeownership by offering payment assistance to increase an applicant's payment ability.

How the USDA Home Mortgage Program Works To guarantee the USDA loan procedure works as planned, the USDA will figure out income restrictions depending upon the location in which an applicant wishes to acquire a house. Loan underwriters are accountable for taking a look at the applicant's gross earnings, earnings from any co-applicants, and any other grownups who plan to live in the household.

The candidate will require to send copies of a minimum of 2 years of Internal Revenue Service tax filings. The primary requirement in securing a USDA home loan is to reveal a clearly visible history of steady earnings. Self-employed candidates might require to provide 3 years of tax returns to develop a clear track record of average earnings.

The Main Principles Of USDA Home Loans

Department of Farming is included with rural housing programs. Reference to this concern goes back to the New Offer, in addition to efforts in the 1930s and 1940s. The objective of the USDA home loan program is to offer a better standard of living and a course to homeownership for rural homeowners.

What Is a USDA Loan? Are You Eligible for One?

Before the production of the FHA and the Real Estate & Urban Advancement (HUD) programs, the U.S. Housing Act of 1949 developed what would become the first consumer USDA rural home mortgage program. This brand-new program then put direct responsibility at the USDA for suitable funding. USDA funding was at first used for on-farm real estate, nevertheless non-rural farm financing was ultimately included order to round out the program's coverage.

To fulfill the objective of much better and more-abundant real estate, the list below provisions of the Real estate Act set the structure for the production of the USDA mortgage program. Title 1 Title I of the Real estate Act financed the clearance of shanty towns under urban redevelopment and renewal programs. Title II Title II of the act increased permission for Federal Housing Administration home mortgage insurance.